Margin Trading: Big Risk for a Big Profit?

Margin trading can allow you to invest more than you could on your own, but it comes with some important risks you should be aware of before getting started.

When purchasing equity stock, most individuals will use a cash account to make transactions. Simply put, this means most retail investors use their own money to make trades in the stock market as opposed to borrowing.

However, it is also possible to buy stocks on margin or with money loaned from a brokerage account. So, how does this work?

What Is Margin Trading?

Margin trading is the practice of using borrowed funds to invest. Essentially, a brokerage firm distributes a margin loan giving you buying power for a given stock.

Just as any other loan tends to operate, there are stipulations the loanee must meet to fulfill the loan. These margin requirements differ, though they often entail interest payments to be paid back later.

Some lenders require that the investor create a margin account, where the investor is required to hold a small amount of cash in this account to serve as collateral. This way, if the investor makes a bad investment with their loan, the lender can recoup some of the loan amount back through the margin account.

How Does it Work?

Say you find an asset's share price to be too expensive. If you have faith in this asset, margin trading allows you to capitalize on that asset without needing the funds to purchase it directly. So, margin trading allows you to take on a full position while only fronting a portion of the amount.

🚩 However, there is also potential for bigger losses. Let's look at 2 examples: one where the investor gains and the other where the investor loses.

Example: gains from trading on margin

Let's say that an investor with $200 in cash believes company XYZ's stock will rise significantly in the near future, but their stock price is currently valued at $300. If this investor is confident they can eventually raise funds necessary to pay off the loan, they will purchase the stock on margin and pay off the loan disbursements later. In this case, they may receive $100 on margin from a lender and purchase a share at $300.

If company XYZ's stock rises to $400 a share and the investor sells, they would repay the $100 loan plus interest, and have a total profit of around $100 (50% profit compared to their $200 of cash).

Example: losses from trading on margin

Let's say that the same investor receives a $100 loan to purchase the $300 stock. After purchasing the stock, the price falls to $250 per share. The investor then sells. After paying back the loan plus interest, they are left with $150 (a 25% loss compared to their $200 in cash).

How Does a Lender Ensure They Are Paid Back?

Many lenders require that an investor hold a margin account. In this account, the investor is required to hold a certain amount of money. For example, if the lender is giving the investor $100, they may require that the investor hold $25 in a margin account.

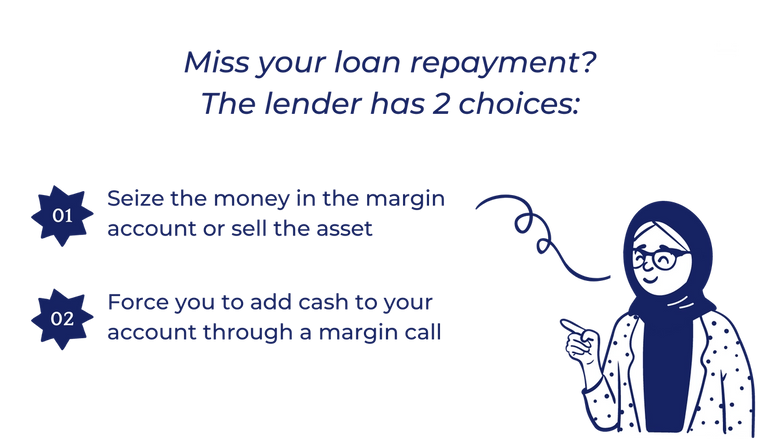

Should the investor make poor investment decisions on margin or miss loan repayments, the lender typically has 2 choices:

1. Seize the money (less common)

The lender is able to seize the money in the margin account or even sell the investor's asset in order to recoup their money.

This is the worst-case scenario. Usually, should an investment on margin underperform, the lender will make a margin call.

2. Make a margin call (more common)

When the total value of an investor's margin account falls below a minimum margin total, which is usually stipulated in the loan contract, the lender will force their investor to raise the account value by depositing additional cash — this is called a margin call.

Conditions such as these are enforced to ensure the lender that the loan will eventually be repaid. If the investor fails to maintain a specific value in their account, the lender will lose faith that the loan will be refunded, and legal repercussions may occur as a result.

Increase Buying Power With Margin Trading

The more money an individual has, the more buying power they have to leverage their investment. Skilled professionals refer to this as "leveraging an investment" because they now have more buying power to pursue capital gains.

Typically, marginal investments are short-term, and therefore the interest payments are relatively unimpactful. However, marginal investments that are not short positions may entail higher interest payments. Since these interest rates are generally dynamic, it may be understood that the longer a position is held, the more interest payments play a role in the health of a margin account.

Let's take a look at some in-depth examples to see how margin trading works.

Example 1

John is an investor who enjoys buying stocks. Up to this point, his investment strategy has been to avoid using borrowed funds and instead utilize his account balance to purchase assets. However, John has recently learned of an emerging pharmaceutical company with well-documented research on a new drug that essentially cures insomnia. Now John, who believes the drug will prove to be a massive success, wants to purchase stock in the company and reap the rewards of the companies inevitable success.

The stock value is currently $50, and John has $1,000 of cash to trade. However, John will be receiving his paycheck soon and believes he will have roughly $5,000 by the end of the week. Unfortunately, John thinks the drug will be released early this week, and by the time he has the $5,000, the stock price will rise tremendously. Puzzled by this complex situation, John ponders and reaches out to his friend Jason for advice. Jason informs John that he can get a loan from his brokerage and buy the stock on margin. John decides to buy $5,000 worth of the stock on margin.

One week later, John receives his paycheck and has enough to pay back his lender. After the week has passed, John checks in on the stock's performance and finds that the asset is currently trading at $125, which is a massive increase from the $50 he bought. Since John spent $5,000 on the stock when it was worth $50, he owns 100 shares of the stock. Now that it is worth $125, he owns $12,500 worth of stock in the company. The loan has accrued $50 of interest in the week, which John pays out of pocket.

Had John decided to purchase only $1,000 worth of the stock, since that's all the cash he had on hand, he would have 20 shares, which would be worth $2,500. Therefore, by purchasing the stock on margin, John made out $4,500 ($12,500-($5,500+$2,500)).

Example 2

As mentioned above, margin agreements entail varying interest rates. The interest rates charged for trading on margin can often become troublesome if the stock's performance underperforms.

To use John's example, if the release of the drug were to underperform and public sentiment displayed an adverse reaction, the price of the stock would consequently fall. Let's say John decided to buy 100 shares on a margin of $50 and the stock plummeted to $10 a share after the disappointing week. The asset's poor performance would mean that John spent $5,000 (plus interest) on a stock worth $1,000.

Therefore, if John sold his shares and used them to pay some of the loan back, he would still owe $4,000 plus any additional interest charges he owes on the loan. This is an example of how risky it may be to buy on margin in certain circumstances.

Advantages and Disadvantages of Margin Trading

Advantages

- Large Potential Gains: If an investor guesses correctly on the performance of a booming stock ahead of time, they can make incredible gains that they otherwise wouldn't have the funds to attain.

- Taking Leverage Positions: Buying on margin allows investors to leverage their purchases into more significant gains. Obtaining a loan and using it to invest in an asset allows an individual to make riskier investments and hedge their bets with funds they otherwise wouldn't have access to.

- Potential to Diversify: Buying on margin may allow an investor to access various investment sectors that they wouldn't otherwise be able to. This newfound ability allows for further diversification of a portfolio. Diversifying a portfolio across varying industries can help mitigate the risk associated with their portfolio. This technique is called leveraging, and it is commonly understood that the more buying power an investor has, the more leverage they have for their portfolio. Therefore, since buying on margin increases buying power, it also provides an investor with significant leverage.

Disadvantages

- Loan Repayment: Buying on margin is a loan, which means the investor will have to pay back the original sum they borrowed as well as interest.

- Falling Victim to Overconfidence: Overconfidence when purchasing stock on margin could lead investors to find themselves in a hole. In other words, guessing wrong on a stock with someone else's money may lead to an unfortunate predicament in which the investor is now locked into interest payments.

- Margin Calls: When a margin account is first created, an agreement will be set in which a minimum value must be maintained within the account. If the value of the assets purchased on margin decreases below that value, the lender will issue a margin call, and the loanee will be forced to deposit funds into the account to meet the metric. This can become a precarious situation for an individual who does not have the funds necessary to raise their account value to that point. Overall, if one is not careful, they may find themselves in a sticky situation in which the debt they owe to their margin lender multiplies quickly and leads to financial turmoil.

How to Get Started

1. Open a margin account

To begin buying on margin, you must open a margin account. Margin trading works with accounts that allow those specific transactions.

There are certain restrictions when it comes to opening a margin account. According to FINRA, most brokerages require that you deposit $2,000 or 100% of the purchase price of the margin security (whichever is less) before you are allowed to trade on margin.

Certain brokerages like Robinhood have to approve investors in order to use margin services. Check your brokerage's specific requirements before attempting to open a margin account.

2. Trade as you would in a regular brokerage account

Once you find a brokerage that will enable you to open a margin account, the transactions work precisely as a regular brokerage account works.

The only difference is that you may have to provide personal information that allows the brokerage to determine whether or not you are eligible to receive a loan and how much the loan disbursements will be.

Key Takeaways

- If the purchase price of a given asset is too pricey for you to purchase with your funds, margin trading may enable you to cover the total value of the stock or fund.

- When investors receive funds for their margin account, they become responsible for interest payments that their loan may accrue. Interest rates vary depending on the brokerage's policies, the loan's size, and the loanee's credit.

- If an investor purchases an asset on margin and the stock underperforms, they will have to pay for the value of the loan (in addition to any interest payments).

The information provided herein is for general informational purposes only and is not intended to provide tax, legal, or investment advice and should not be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation of any security by Candor, its employees and affiliates, or any third-party. Any expressions of opinion or assumptions are for illustrative purposes only and are subject to change without notice. Past performance is not a guarantee of future results and the opinions presented herein should not be viewed as an indicator of future performance. Investing in securities involves risk. Loss of principal is possible.

Third-party data has been obtained from sources we believe to be reliable; however, its accuracy, completeness, or reliability cannot be guaranteed. Candor does not receive compensation to promote or discuss any particular Company; however, Candor, its employees and affiliates, and/or its clients may hold positions in securities of the Companies discussed.