5 Main Types of Institutional Investors

Institutional investors differ greatly from your average investors. What they are and the 5 main types you should know.

In the finance world, investors are usually divided into two groups: retail investors and institutional investors.

If you’re an individual, buying and selling your own stocks, bonds, or other securities and building your own portfolio, you’re a retail investor.

An institutional investor, on the other hand, is an entity that invests money on behalf of other people. Because of their size and influence, institutional investors greatly impact financial markets and the companies they invest in.

The Basics

What Is an Institutional Investor?

In short, an institutional investor is a company or organization that pools the funds of multiple investors and participates in trading in the financial markets.

An institutional investor is always a legal entity: for example, the company, organization, or enterprise managing a private equity fund is the institutional investor, not the PE fund itself.

What Does an Institutional Investor Do?

An institutional investor manages a significant number of funds and is at its core a professional entity, conducting asset management and investment management. Institutional investors buy, sell and manage stocks, bonds, ETFs, and other securities or investment vehicles, such as fixed-income investments.

Institutional investors invest the assets they manage in a range of different classes. According to McKinsey’s 2017 report on the industry, approximately 40% of assets were allocated to equity, and 40% to fixed income. Another 20% were invested in other investments like real estate, private equity, and hedge funds. These percentages can vary significantly from institution to institution, however.

5 Main Types of Institutional Investors

While there are many types of institutional investors, there are a few that make up a particularly large part of the institutional investing community. Here’s an overview of some of the main types of institutional investors:

Institutional Investors vs. Retail Investors

The most obvious difference between a retail investor and an institutional investor is that an institutional investor is a company or organization rather than an average individual.

Resources & Knowledge

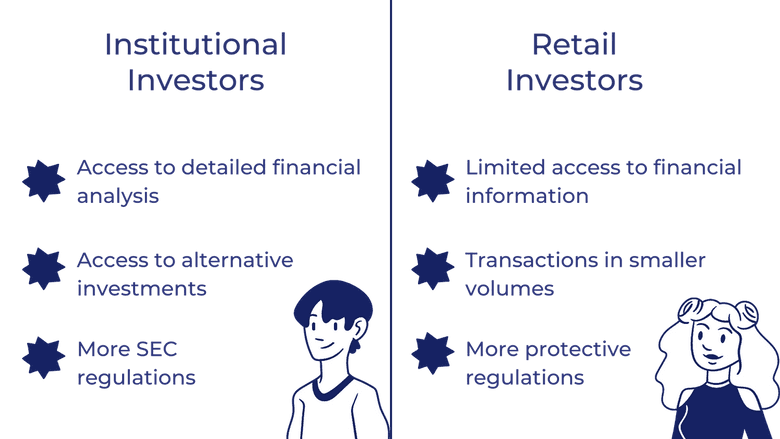

Institutional investors generally have more resources and specialized knowledge than retail investors do, and will often incorporate detailed financial analysis and ESG (environmental, social and corporate governance) factors into their investment decisions.

They often have access to alternative investment opportunities not available to the average retail investor, and some institutional investors might also have access to corporate insiders, such as a company’s CIO or other executives who could provide additional intelligence.

Amounts Traded

Retail investors are generally non-professional investors — they can be average people managing their own personal brokerage or savings accounts. These investors usually execute their trades through traditional or online brokerage firms, and generally trade in much smaller amounts than institutional investors do.

Retail investors are more likely to invest in smaller companies' stocks than institutional investors because smaller companies often have lower price points. Because their trades are usually smaller, retail investors might also pay higher fees or commissions when trading.

Retail investors and institutional investors usually buy securities in different quantities, too. Typically, institutional investors will trade in much larger volumes: retail investors might buy and sell stocks in lots of 100 shares, while institutional investors might buy or sell in lots of 10,000 shares or more.

Rules & Fees

Institutional investors are also subject to fewer protective rules and are entitled to preferential treatment and lower fees, as they’re generally considered to be more market-savvy and qualified than the average individual investor (retail investor). It’s assumed that these asset managers are more knowledgeable, and therefore better equipped to protect themselves than retail investors are.

Markets

Although both retail and institutional investors are active in a range of different financial markets, some markets might skew more towards institutional investors because of the types of securities traded and the way transactions occur.

Impact and Influence

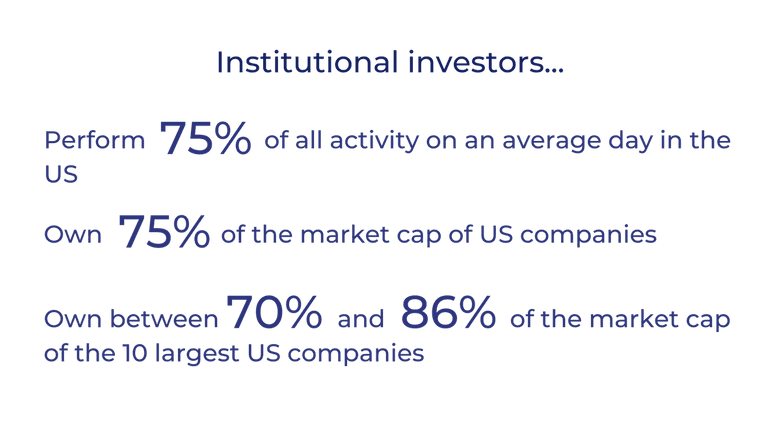

Institutional investors account for the majority of stock market activity, usually around at least 75% of all activity on an average day in the United States.

Institutional investors are highly influential in the financial markets. Because they perform the majority of transactions on major exchanges, they are a major force behind market supply and demand. In turn, they have a strong influence on the prices of securities (like stocks) and the valuation of companies.

It’s also estimated that institutions own over 75% of the market cap of companies in the U.S. broad-market Russell 3000 index and large-cap S&P 500 index, and between 70% and 86% of the market cap of the 10 largest companies in the United States.

The capital managed by institutional investors is often referred to as “smart money.” This term refers to capital managed by those considered experienced, well-informed, or especially qualified.

In essence, it’s believed that this invested capital will perform more successfully because it’s invested with a better understanding of the market or with intel not accessible to a regular investor. Institutional investors often meet personally with company executives and analyze and evaluate entire industries and companies in depth before making specific investment decisions.

Risks and Challenges

Because of their size, influence, and scale, institutional investors often contend with greater risks than retail investors. These risks — like stock volatility, inflation, and the risk generally associated with doing business — aren’t necessarily unique to institutional investors, but institutional investors are less protected than retail investors.

The development of technology can also introduce both new opportunities and new challenges to institutional investors: information now spreads more quickly than ever and can be difficult to manage, especially on a large scale. There is also the possibility of fraud related to trading and general security risks as many institutional investors deal with large quantities of sensitive or private information.

Another challenge to institutional investors is the increasing pressure to invest more responsibly and to take into account social and environmental factors when investing. Many institutional investors have specifically increased their focus on ESG investing, with many reporting that they fully integrate ESG factors into research, security selection, and portfolio construction.

Takeaways

- Institutional investors control a significant amount of all financial assets in the United States, and therefore have a significant influence on all financial markets — an influence that has only grown over time

- Institutional investors have more government regulations based on their influence over the markets

- As these institutions continue to grow, so will their holdings and influence

The information provided herein is for general informational purposes only and is not intended to provide tax, legal, or investment advice and should not be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation of any security by Candor, its employees and affiliates, or any third-party. Any expressions of opinion or assumptions are for illustrative purposes only and are subject to change without notice. Past performance is not a guarantee of future results and the opinions presented herein should not be viewed as an indicator of future performance. Investing in securities involves risk. Loss of principal is possible.

Third-party data has been obtained from sources we believe to be reliable; however, its accuracy, completeness, or reliability cannot be guaranteed. Candor does not receive compensation to promote or discuss any particular Company; however, Candor, its employees and affiliates, and/or its clients may hold positions in securities of the Companies discussed.